Yes, if the sum is large, it will be easier to obtain as a secured loan than an unsecured loan. Loans are less risky when an asset is used as collateral, therefore your chances of approval may be better.

Secured car loans

At CarLoans.com.au we can get you into your next car at the best possible rate. We choose from hundreds of secured car loans offered by almost 30 different lenders to find the perfect solution for your individual needs.

With expert brokers on hand, we’ll do the hard work from you, all the way from application through to settlement.

We can help you every step of the way.

We’ll save you from all the stress while saving you valuable time and money too—a complete one-stop shop! Our car loan specialists are here to help you, from navigating the minefield of lender requirements to negotiating and arranging the settlement with the lender.

Best possible deal

Our experienced car loan specialist will fight for you and save you money.

Bad credit

We can find you good value finance regardless of your personal circumstances or credit history.

Leading lenders

We select products from only the best lenders who meet out strict criteria for price, service and ethics.

Easy process

We take the hassle out of getting a car loan.

How to apply

CarLoans.com.au takes the hassle out of applying for a secured car loan.

Our four-step process saves you time and gets you behind the wheel fast.

- Describe your needs and apply online or over the phone.

- We'll find you the best finance available.

- We'll arrange the application and the settlement.

- Drive away in your new car!

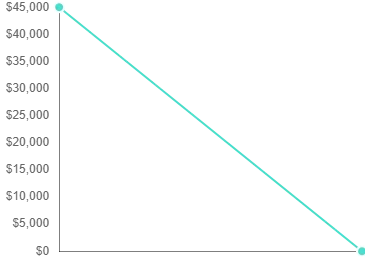

Calculate your car loan repayments

Your estimated repayments are

$625

$45,000

$0

$45,000

What is a secured car loan?

A secured car loan is one that is secured against the vehicle that you acquire with the money you borrow. The lender uses the car as collateral, which means that if you don't make the agreed-upon repayments, the lender can seize the vehicle and sell it to recoup their money.

This security means the lender will typically give a reduced interest rate on the loan compared to unsecured car finance, making secured car loans the most popular type of car finance.

In contrast, an “unsecured” car loan is not secured against the vehicle. As a result, it is effectively the same as a personal loan. If you fail to make your repayments, the lender will need to take you to court to recover their funds. To compensate for this risk, lenders typically charge a higher interest rate for these loans, impose additional fees, and are less flexible with who they lend to.

Benefits of a secured car loan

The key benefit of a secured car loan is that you can get a cheaper car loan interest rate, which means borrowing money to buy a car will be less expensive.

A secured loan also has the following advantages:

-

Because of the lower risk to the lender, you may be approved for a larger loan.

-

Some lenders allow longer payback periods for secured loans than they do for unsecured loans.

-

Because of the collateral, it may be easier to get approval for your car finance.

Secured vehicle loans: fixed vs. variable

Fixed Rate

These personal car loans have a fixed rate which ensures that your loan repayments will not vary for an agreed period, which for a car loan is generally the full loan term. This means you know precisely how much you'll pay each month so it easier to budget. Even if interest rates rise unexpectedly, this kind of loan will be unaffected.

Variable Rate

A variable-rate car loan comes with an interest rate that can rise or fall over the course of the loan term, at the lender’s discretion. With a variable-rate loan, there is the potential to save money if the rate falls, but you could also lose out if it rises and be forced to make higher repayments. Like a variable rate home loan, a variable rate car loan gives you more flexibility to make extra repayments or pay off the loan early.

Fixed-Rate vs. Variable-Rate

So, how do you choose between them? The answer is highly dependent on your personal preferences as well as your financial position.

If you don't want to take the risk of a variable rate, which might rise and leave you with higher loan repayments, a fixed-rate car loan is a better option.

It's also ideal to fix if you expect your income to be stabled for the life of the loan. On the other hand, if you predict a promotion or bonus, you may want to make extra payments to pay off the debt sooner, in which case a variable car loan may be more suitable for you.

Make sure to complete a thorough analysis of your finances before making a decision, or for more information, read our guide on fixed vs variable car finance.

What to Think About When Getting a Secured Car Loan

A variety of secured car loans are available from different of lenders. The ideal secured vehicle loan for you will depend on your financial status and the length of loan you desire. Here are a few things to consider when assessing a loan.

The interest rate

Secured car loan rates impact your monthly payments and vary substantially amongst lenders. Be sure to examine comparison rates that include the complete cost of the loan before applying.

Fees

These can include one-time expenses such as establishment fees, as well as recurring fees such as loan service fees. To be sure you're receiving a decent deal, compare fees in addition to interest rates and loan features.

The duration of the loan

Lenders specify certain loan periods that you may choose from (typically one to five years for fixed-rate loans and one to seven years for variable rate loans). Check to see whether you can repay the loan over a time that fits your budget.

The loan's minimum and maximum amounts

The average minimum loan amount is $5,000, with maximum loan amounts varying widely amongst lenders. Some lenders don't have a maximum loan amount and instead judge on a case-by-case basis. Keep this in mind while deciding which vehicle to purchase.

Additional payments

Some lenders allow you to make extra repayments to pay off your debt faster. If you think you'll be able to contribute more money to your loan, make sure to factor this into your comparison. Keep in mind that some lenders will charge fees if the loan is paid off early, so try to look for a loan that doesn't have these fees.

Additional features

Loans come with a variety of features to assist you in managing them more effectively. Some lenders include cheap car insurance with their loans, while others provide car-finding services.

Frequently asked questions

Arrange a Call

Fill out the following details and one of our car loan specialists will be in contact.

Finance

Why use a car finance broker?

With the help of an experienced, qualified finance broker, you don’t need to stress so much about the paperwork and application for your car loan. As your finance broker could advise what is required and guide you through the processes and maze of paperwork.

25 Mar, 2025

Car Advice

How to buy a car online

If you are one of the many Aussies who is wondering “can I buy a new car online”, then this article is for you.

25 Mar, 2025

Finance

5 environmental benefits of green cars

Green cars are vehicles that are considered more eco-friendly compared to standard gas or petrol-powered cars because of their reduced emissions. In addition to their positive environmental impacts, there are other benefits to owning a green car. Learn more!

24 Oct, 2024

Finance

How to reduce your car loan repayments

24 Oct, 2024

Car Advice

Buying Used Electric Vehicles

20 Sep, 2024

Car Advice

Do you need a deposit for a car loan?

30 Aug, 2024